The coronavirus-induced recession has seen countries that were already battling a skyrocketing national debt plunge into more crisis.

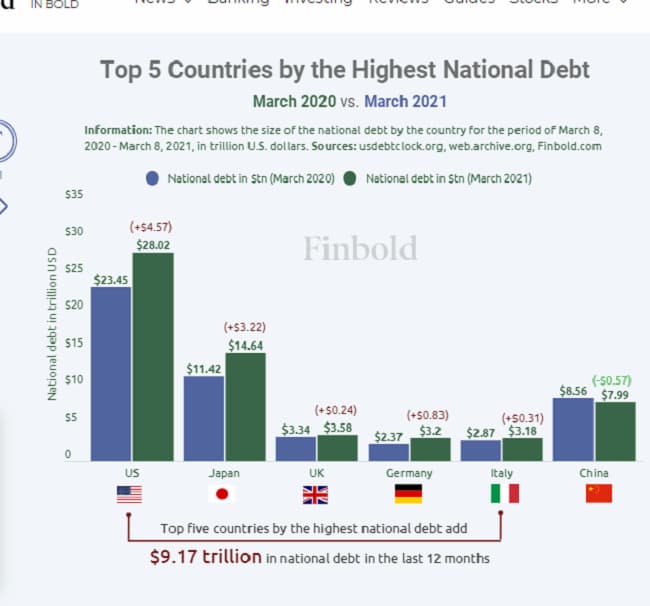

Data analyzed by Finbold indicates that the top five countries globally with the highest public debt added $9.17 trillion between March 2020 and March 2021. The United States tops with the debt growing by $4.57 trillion from $23.45 trillion to $28.0.2 trillion.

Japan’s Public Debt

Elsewhere, Japan’s public debt has grown from $11.42 trillion to $14.64 trillion. Cumulatively, the two countries have added $7.79 trillion in debt. Interestingly, the analysis shows that China’s national debt dropped by $0.57 trillion from $8.56 trillion to $7.99 trillion among the selected leading economies.

Top 5 Countries With National Debt

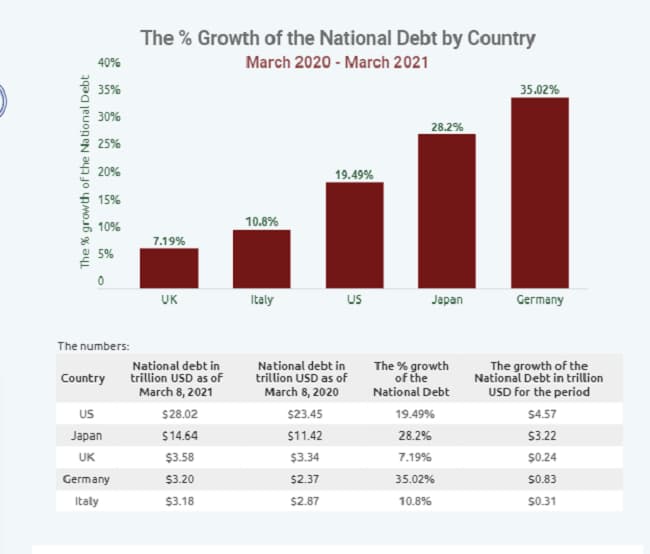

In terms of the country’s national debt percentage growth, Germany tops with 35.02%, followed by Japan at 28.2%, and the U.S. ranks third at 19.29%. Italy’s debt grew by 10.8%, with the UK standing at 7.19%.

US debt crisis complicated by COVID-19 response

The record surge in national debt for the covered countries is mainly due to the coronavirus pandemic. The health crisis triggered the most profound economic downturn, with millions of people losing jobs and businesses temporarily or permanently closed; hence, revenues shrunk while spending soared.

Even before the pandemic, the United States was already battling a huge national debt crisis. The situation was further complicated after Congress approved several stimulus packages for relief, widening the debt. Furthermore, the low-interest rates meant that the US had to shoulder a heavier debt burden.

Japan

Similarly, Japan’s high national debt stems from the country’s response to the health crisis. The stimulus spending also put more pressure on the already dire public debt.

China’s pandemic response helps lower public debt

Despite being the virus epicenter, it was controlled swiftly, with economic activities resuming normally. There was a balance between spending and revenue generation, meaning the deficit amount was low over the last 12 months.

China was also able to inject more money into the economy after becoming a key exporter of products needed to fight and curb the coronavirus pandemic. For instance, Asian nations exported a significant amount of face masks and ventilators to countries that lacked the capacity to produce their own.

Away from the pandemic response, China’s declining public debt ties down the policy. In recent years the country has become less reliant on using credit to handle economic slowdowns. Amid the pandemic, policymakers were even reluctant to over-use debt to hit growth targets.

Overall, most countries globally have enacted a massive amount of monetary and fiscal stimulus to prevent a deep and prolonged recession, in return increasing the public debt burden. However, it appears there has been little effort to balance the coronavirus response with solving the national debt crisis.

The surging national debt for countries like the US is worrying since it has since surpassed its Gross Domestic Product (GDP) of $21.59 trillion, according to the U.S. National Debt Clock. It is an indicator the country might have problems repaying the loans.

With the debt in the unstainable territory for some countries, it might generally impact the government’s ability to tackle future economic downturns.

{kind=link}