Business conditions in Nigeria’s private sector improved modestly midway through the third quarter, but the rate of growth slowed from that seen in July, 2022.

Softer upticks were recorded in output, new orders and purchasing activity while employment rose at a quicker pace. At the same time,

overall input price inflation rose at the second-fastest rate on record while sentiment moderated to the weakest since last November.

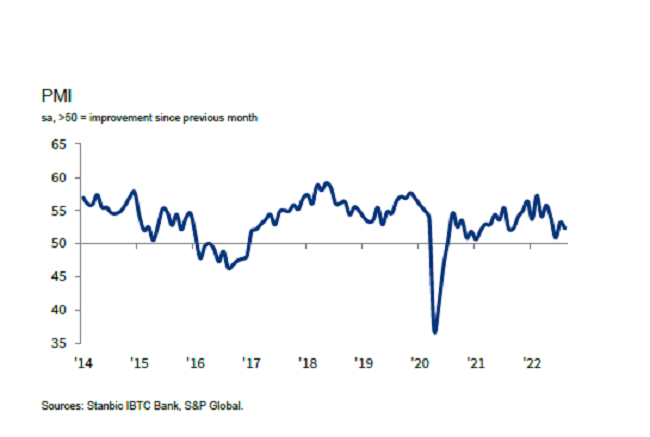

The headline figure derived from the survey is the Purchasing Managers’ Index™ (PMI®). Readings above 50.0 signal an improvement in business conditions on the previous month, while readings below 50.0 show a deterioration.

The headline PMI registered at 52.3 in August, down from 53.2 in July, signalling another improvement in business conditions. That said, the rate of growth was weaker than the long-run series average.

New orders rose for the twenty-sixth month running in August which panellists linked to general improvements in customer demand. The rate of growth did ease from July, however, amid elevated prices.

Higher sales underpinned a second successive uptick in output in the Nigerian private sector. The rate of growth was broadly in line with that seen in July but was softer than the long-run series average.

Of the four monitored subsectors, three registered output growth. Agriculture topped the rankings, followed by wholesale & retail and services, respectively. Manufacturers, meanwhile, recorded a fall in output levels during August.

Despite slowdowns in output and new order growth, firms added to their headcounts at a quicker pace in August. The overall rate of job creation was modest and the highest for three months.

Subsequently, firms continued to reduce their backlogs, but the rate of decline was fractional amid difficulties sourcing some key inputs.

Advance payments led to quicker supplier delivery times in August. In fact, vendor performance improved to the greatest extent in three months. Quicker lead times allowed firms to add to their inventory holdings. Stocks of purchases rose at a slower pace to that seen in July, however.

On the price front, higher commodity and transportation expenses exerted upward pressures on purchase costs. At the same time, firms raised their staff wages to motivate their workforces and in light of higher living expenses. The overall rate of input price inflation was the second-fastest in the survey’s history, surpassed only by that seen in November 2021.

Looking ahead, firms remained optimistic of output growth in the year ahead, as has been the case since the survey began in January 2014, but the degree of positivity was the weakest for nine months.

{kind=link}